Having a variable or fixed mortgage is a personal decision. You should be the one to make this decision and not your banker, or your mortgage broker, not your real estate agent and not someone who is not personally interested.

You should do what makes sense for you and your finances. This should be talked through with your partner and you should find an approach you are both comfortable with.

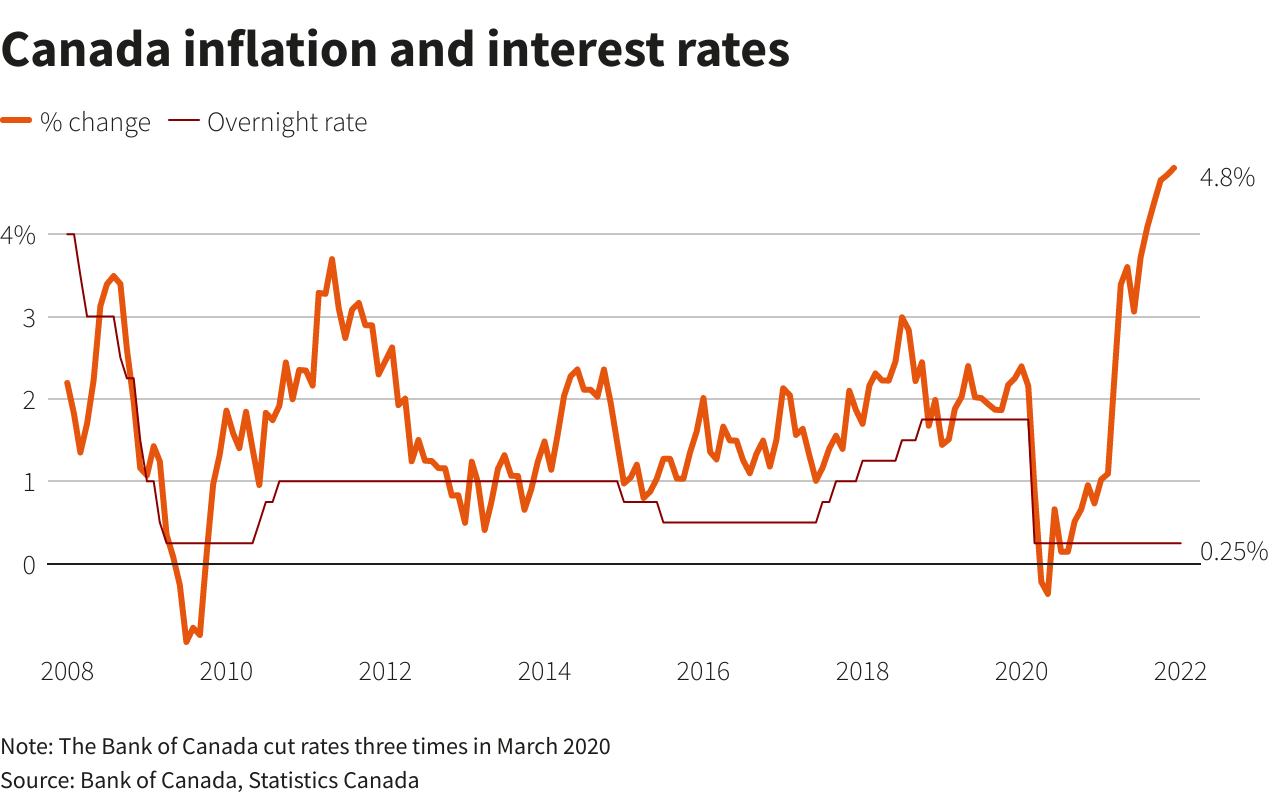

Some mortgage borrowers’ confidence in variable rates may be tested as the Bank of Canada’s overnight target rate starts its inevitable climb upwards, perhaps as early as this week.

Many people are starting to wonder if they should make the switch to a fixed rate—all the news seems to imply such a choice is becoming imminent. This is a legitimate question, and it’s one many mortgage borrowers have already asked.

What Should You Do?

When you chose a variable-rate mortgage, you understood that the rate would vary. This means the rate may go up or down from time to time. The rate fluctuations are impossible to predict and it is guaranteed they will not remain constant for the duration of your mortgage term.

However, after years of falling and flat rates, this could be the first time some borrowers have felt a rate increase.

If you have been locked in a fixed mortgage – fluctuations are not something you know.

Why should you choose a fixed-rate mortgage?

Fixing your mortgage rate keeps your finances in check monthly and keeps everything predictable. There is no shame, and no one can tell you it is the wrong decision. Fixed mortgages are for those who do not like risk or fluctuations.

For the risk-averse homeowner, a 5-year fixed makes sense for most long-term borrowers with less established finances. It also insures against the small but real risk that inflation is being drastically underestimated.

A fixed rate can be beneficial for traditional property investors with a five-year plus holding period.

Where are interest rates actually headed?

To us, it appears that rate hikes and other bank related fluctuations are as predictable as the weather.

The Bank of Canada drastically cut its overnight target rate in the early days of the pandemic, from 1.75% to 0.25% in March 2020. As a result, the prime rate—upon which variable rates are based—fell from 3.95% to 2.45%, where it’s been ever since. And suddenly, a slew of homeowners experienced the thrill of variable-rate mortgages below 2% for the first time ever.

Since then, the party has been loud and boisterous, with more people choosing variable-rate mortgages than at any time in memory. And variable-rate mortgages today are routinely available under 1.50%, with some even under an unimaginable 1%. Current fixed-rate offerings of 2.79% or more are rendered pale in comparison.

Back to the Question – What Should You Do?

We refer back to our opening paragraph, having a variable or fixed mortgage is a personal decision. You should be the one to make this decision and no one else.

As always, if you need help buying or selling your house do not hesitate to contact Gregg Bamford or Ryan Bamford.